It was just a few years ago we were debating which had to happen first: do we need to build more clean energy generation to drive down the cost of it, incentivizing consumers to switch to electric heat and transport? Or, do we electrify everything first to justify that build-out of clean energy generation? It was a chicken-and-egg dilemma because electricity demand growth had stayed relatively flat for the two decades prior, meaning no explicit upwards or downwards trend pushed the thinking one way.

Well, that sure has changed.

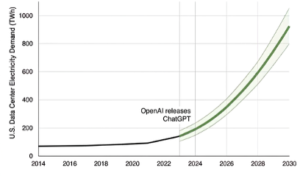

When OpenAI released ChatGPT in 2023, it was the beginning of the end of the debate. We now know for certain electricity demand growth is expected to skyrocket with the buildout of AI datacenter infrastructure, to the tune of 177–192 TWh in 2024 to 800 TWh or higher by 2030 according to most recent forecasts by the Electric Power Research Institute (EPRI). This forecast is 60% higher than a 2024 forecast provided by EPRI, insisting the expectations for our AI datacenter era power needs are only growing by the month.

(Image adapted from EPRI, February 2026)

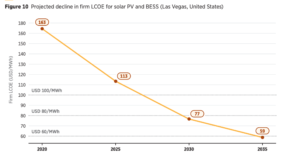

Happening in parallel to unprecedented demand for power is the falling Levelized Cost of Energy for renewables (mainly defined as solar or wind paired with a battery storage system) which is expected to continue to fall. Meanwhile, US combined-cycle gas turbines have doubled in cost as data center demand initiated a supply crunch. The shift is a perfect storm of falling capital costs of the technology, better efficiency, government incentives and tax credits, and AI data center buildout.

(Image source: World Resource Institute, September 2025)

While renewable generation has risen dramatically—with utility-scale solar now accounting for more than half of all new power capacity coming online-—we still rely heavily on fossil fuels to fill the gaps when the sun isn’t shining or the wind isn’t blowing. Fossil fuel power plants have historically been the generators of choice because they can burn exactly the amount of fuel needed at any point of the day to meet energy demand.

Battery energy storage is what changes that dynamic. By absorbing excess energy during high-generation periods of renewable energy, that stored power can be discharged during low- or no-generation periods. While thought to be far-off, 24/7 clean energy through this strategic pairing is possible and already happening in areas of the world. The International Renewable Energy Agency (IRENA) published a report last month, stating that “In high-quality resource regions, firm renewable electricity has crossed the threshold of cost competitiveness with new fossil fuel generation, to provide 24/7 clean energy.”

So with power demand increasing, clean power costs falling, gas costs increasing, and 24/7 clean power demonstrating its viability, let’s ask ourselves the question: how much energy storage do we need for a 100% clean U.S. electric grid in the AI Era?

A helpful starting point is a recent forecast from the National Electrical Manufacturers Association (NEMA). In its 2043 outlook, NEMA estimates a U.S. grid with 2,395 GW of installed generating capacity, including 303 GW of standalone battery storage, 568 GW of solar, 408 GW of wind, 117 GW of nuclear, 533 GW of oil and gas, and 57 GW of coal.

NEMA’s forecast is not a 100% clean electricity scenario. It is a high-demand grid scenario. It shows what the U.S. power system may need to serve rising electricity consumption from AI data centers, electrified transportation, industrial load growth, and broader electrification.

So if we want to convert NEMA’s high-load 2043 grid into a 100% clean grid, the question becomes: what replaces that reliability function?

A simple way to think about it is this: NEMA’s 303 GW of battery storage is the storage requirement for a future grid that still has nearly 600 GW of fossil fuel capacity. A 100% clean version of that same grid would almost certainly require more storage, more clean firm generation, more transmission, more demand flexibility, or some combination of all four.

This is where the difference between “more batteries” and “enough clean flexibility” becomes critical.

Short-duration lithium-ion batteries are already proving their value. They are excellent at shifting solar power from the middle of the day into the evening, providing fast-response grid services, reducing renewable curtailment, and helping meet peak demand. That is why battery storage deployment has accelerated so rapidly and why NEMA expects standalone storage to become one of the largest resource categories on the grid.

But the final stretch toward 24/7 clean electricity is harder than the first stretch. Once renewables supply a very high share of electricity, the system does not just need four-hour storage. It needs storage and clean firm resources that can cover longer renewable shortfalls, localized grid constraints, seasonal mismatches, and reliability events that do not fit neatly into a single afternoon-to-evening cycle.

This is also why measuring storage only in gigawatts can understate the scale of the challenge. A 303 GW battery fleet with four hours of duration represents about 1,200 GWh of battery storage energy capacity. At eight hours, it represents about 2,400 GWh. At twelve hours, it represents more than 3,600 GWh. The same amount of power capacity can represent very different levels of grid resilience depending on duration. For reference, the U.S. currently sits at about 61 GW / 174 GWh of energy storage capacity.

A few hundred GW of storage may be what a high-load, partially fossil-backed grid needs. A 100% clean grid in the AI era likely needs storage and clean firm resources at a much larger effective scale — potentially hundreds of additional gigawatts of storage-equivalent reliability when accounting for the fossil capacity that must be replaced, the longer durations required, and the regional nature of new load growth.

That is the real storage challenge ahead. Not whether batteries can help. They already are. The question is what kinds of batteries, at what durations, with what safety profiles and supply chains, can scale far enough to finish the job.

This remains a daunting task, and it means we must explore high-performance, low-cost, safe opportunities to deploy storage safely near load centers with resilient domestic supply chains, without compounding lithium/cobalt/nickel/graphite dependencies, and potentially at longer durations than the current lithium-ion sweet spot.